How Carbon Credits Work, and Why Brazil Holds the World’s Best Hand

eyesonbrasil

Somewhere in the Brazilian state of Acre, a hectare of rainforest that didn’t get cut down this year just became a financial instrument. It has a serial number, a registry entry, and a buyer somewhere in Rotterdam or São Paulo who will use it to make a claim about their company’s emissions. That transformation — a tree left standing, becoming a tradable unit of climate math — is the entire carbon credit economy in miniature. It’s an elegant idea and a genuinely difficult engineering problem, and Brazil is currently the place where both are being tested at the largest scale on Earth.

What a Carbon Credit Actually Is

A carbon credit is a certificate representing one metric ton of carbon dioxide (or its equivalent in another greenhouse gas, “CO2e”) that was either kept out of the atmosphere or removed from it. Credits move through two very different markets:

Compliance markets are created by law. Governments cap how much a regulated industry may emit (the EU Emissions Trading System is the classic example) and let companies trade allowances among themselves. If you emit less than your cap, you can sell the difference; if you emit more, you have to buy.

Voluntary markets exist outside any legal mandate. A company that wants to say it has “offset” its emissions buys credits generated by projects elsewhere — a wind farm that displaced coal power, a cookstove program that cut wood burning, or a forest that stayed intact. This is the market where nearly all of Brazil’s rainforest and reforestation projects operate, at least for now.

Both markets rest on the same underlying logic: an emission reduction here can substitute for a reduction there, because a ton of CO2 has the same warming effect no matter where on the planet it was avoided.

How the Number Gets Calculated

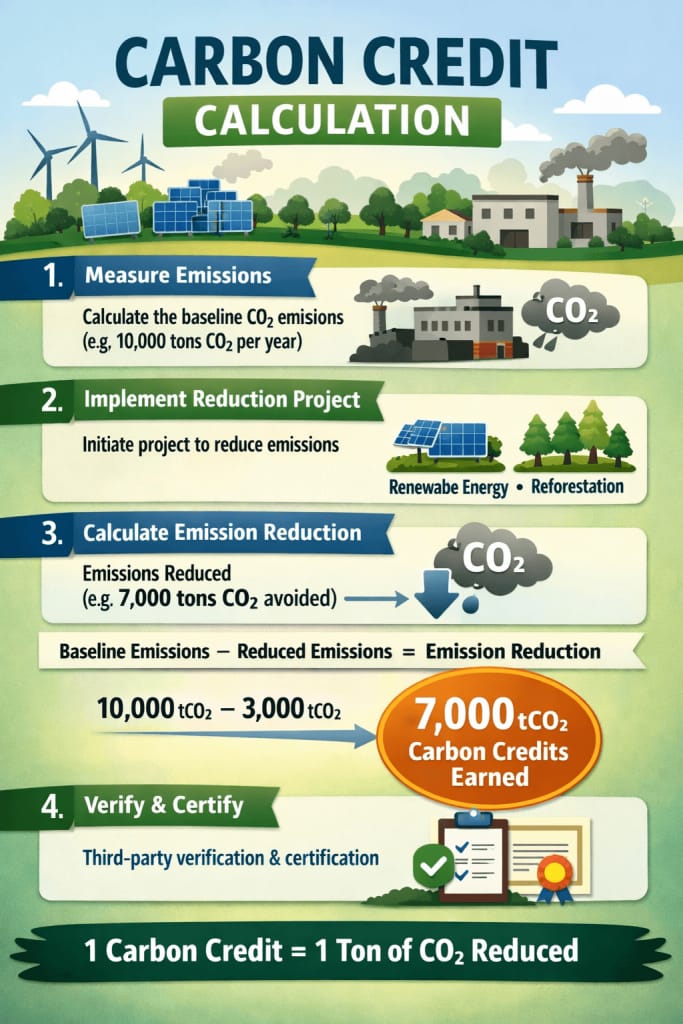

This is where the elegant idea meets the hard engineering. A credit isn’t awarded just because good things happened at a project site — it’s awarded because things happened that would not otherwise have happened, and that calculation runs through several layers.

1. The baseline. Project developers first model a “business as usual” scenario: how much deforestation, or how many emissions, would have occurred without the project. This baseline is the yardstick against which everything else is measured.

2. Additionality. The project has to prove its impact is additional — that the carbon benefit wouldn’t have happened anyway, whether from existing law, market trends, or a landowner’s own plans. A protected area that was never actually under threat of logging can’t legitimately generate credits, because nothing is being avoided.

3. Actual performance vs. baseline. Using satellite monitoring, ground surveys, and increasingly machine-learning models, verifiers compare what actually happened on the ground to the baseline projection. The gap between them — tons of CO2 avoided or removed — is the raw credit volume.

4. Leakage. If protecting one forest simply pushes the loggers next door, the project hasn’t achieved a net reduction — it’s relocated the problem. Rigorous methodologies discount credit volumes to account for this displacement.

5. Permanence and the buffer pool. A forest can burn down or be cleared years after credits were sold. To cover this risk, a percentage of credits — often 10 to 20% — is withheld in a non-tradable “buffer pool” that can be canceled if a project reverses.

6. Verification. Independent auditors, accredited under a standard such as Verra’s VCS or Gold Standard, check the math and the monitoring data before a registry actually issues tradable units.

The formula, stripped down, looks like:

Credits issued = (Baseline emissions − Actual emissions) − Leakage − Buffer pool reserve

Each variable is a judgment call built on models, and that’s precisely where the system has drawn its sharpest criticism. A widely cited 2020 study in PNAS examined a set of voluntary REDD+ projects in the Brazilian Amazon and found that their crediting baselines assumed consistently higher deforestation than counterfactual forest loss estimated through statistical comparison sites, meaning some projects had likely overstated their climate impact. The market has been racing to fix this: Verra’s newer VM0048 methodology tightens baseline-setting substantially, and modeling suggests emissions-avoidance estimates could fall 30 to 90% for some Brazilian projects as they transition to the new standard — a sign the industry is correcting toward rigor, even at the cost of shrinking credit supply from weaker projects.

Brazil’s Ambitious Bet on Standing Forests

Few countries have more riding on getting this right. The Amazon alone holds roughly 56.8 billion metric tons of carbon above ground, with Brazil containing more than 32 billion tons of that total — a carbon stock worth more than one and a half times the entire planet’s annual CO2 emissions. Several Brazilian initiatives illustrate where this market is heading.

Envira Amazonia, Acre. This project protects roughly 39,000 hectares of rainforest in the western Amazon, a region under mounting pressure from highway expansion and advancing cattle and soy frontiers. It has earned a rare “Triple Gold” rating across climate, community, and biodiversity criteria, and is developed by CarbonCo with independent auditing by Rainforest Alliance under both VCS and CCB standards — the kind of layered verification the market is increasingly demanding.

Jurisdictional REDD+ (JREDD+) and the TREES standard. Rather than certifying individual forest patches, Brazil is testing carbon accounting at the scale of entire states. Under this model, the four most advanced states — Acre, Mato Grosso, Pará, and others — could collectively issue around 1.05 billion TREES-standard credits for deforestation reductions achieved between 2023 and 2030, potentially generating $10–20 billion in revenue at $10–20 per credit. Because it operates at state level, this approach is harder to game through leakage than a single-project boundary, and it plugs more naturally into the UN’s own accounting architecture.

Re.green’s Bom Futuro concession. In March 2026, Brazil awarded its first long-term public land concession specifically for Amazon reforestation backed by carbon finance, granting the startup Re.green rights to restore 59,000 hectares of degraded land. Unlike avoided-deforestation projects, this generates removal credits — carbon actively pulled back out of the atmosphere as forest regrows — a category regulators and buyers increasingly favor because it’s less dependent on modeling a hypothetical baseline.

Brazil’s own regulated market (SBCE) and the Amazon Fund. Brazil’s compliance carbon market was signed into law in December 2024, and the Amazon Fund — financed by sovereign donors — has crossed R$4.98 billion in donations, disbursing over R$1 billion in approved projects in the first half of 2025 alone. Hosting COP30 in Belém in November 2025 gave Brazil a stage to press the case, and the summit produced a $5.5 billion Tropical Forest Forever Facility alongside 27 Indigenous land-demarcation advances.

The backdrop makes the timing meaningful: Brazilian Amazon deforestation fell roughly 50% between 2022 and 2025, reaching its lowest annual level in eleven years. Falling deforestation is unambiguously good news — but it also means the “avoided” baseline that many credits are priced against keeps shifting, which is exactly the kind of moving target that makes rigorous methodology so important.

How This Connects to the Paris Agreement

Carbon credits aren’t just a private-sector accounting trick sitting alongside international climate policy — the Paris Agreement was written with a market mechanism built directly into it, under Article 6.

Article 6.2 lets countries trade “internationally transferred mitigation outcomes” (ITMOs) bilaterally. If Brazil generates a verified emissions reduction and sells it to, say, Switzerland, Switzerland can count it toward its own Paris pledge — its Nationally Determined Contribution, or NDC.

Article 6.4 established a centralized, UN-supervised crediting mechanism — the successor to the Kyoto Protocol’s Clean Development Mechanism — through which public and private actors can generate emission-reduction or removal credits that either the host country counts toward its own NDC, or transfers to a buyer country. Its key operating rules were finalized at COP29 in Baku in 2024.

The mechanism everyone in this space discusses most is the corresponding adjustment. Because both a seller and a buyer country have their own emissions targets, a single ton of avoided CO2 can’t legitimately be claimed by both. So when a country sells a credit, one ton is added back to the seller’s own emissions ledger while one ton is subtracted from the buyer’s — ensuring the reduction is booked exactly once in the global accounting system, even as the credit itself changes hands.

For Brazil, this is the frontier its jurisdictional REDD+ programs are being built toward. A voluntary-market credit sold to a corporate buyer today doesn’t (yet) require a corresponding adjustment to Brazil’s NDC. But as state programs like Acre’s and Pará’s mature toward Article 6.2 and 6.4 eligibility, those same forest credits could start counting in the formal architecture of the Paris Agreement itself — turning Brazil’s standing forests from a voluntary-market curiosity into a load-bearing piece of how the world actually tracks its progress against 1.5°C.

The Honest Caveat

None of this erases the hard questions. Baselines can be gamed, verification is only as good as the standard behind it, and a paper from PUC-Rio examining additionality across the Amazon found that while non-forest and under-pressure regions showed high rates of additionality, already-forested regions showed significantly lower rates — meaning not every hectare protected on paper was ever really at risk. The market is visibly responding: tighter methodologies, jurisdictional-scale accounting, and a shift toward the highest-integrity, most heavily audited projects.

Carbon credits will not, by themselves, solve climate change. What they can do — if the accounting holds up to scrutiny — is put a real price on the world’s remaining intact forests, and give a country like Brazil a financial reason to keep 32 billion tons of carbon exactly where it already is: in the ground, and in the trees.

This article is a sensitive-topic overview and reflects publicly available information on carbon markets and Brazilian forest-carbon programs as of mid-2026; carbon market rules, methodologies, and project statuses continue to evolve rapidly.